BOOKKEEPING Form 1 Topic 3

CLASSIFICATION OF ACCOUNTS

It is necessary to know the classification of accounts and their treatment in double entry system of accounts. Broadly, the accounts are classified into three categories:

- Personal accounts

- Impersonal

- Real accounts

- Tangible accounts

- Intangible accounts

Let us go through them each of them one by one.

Difference between Personal and Impersonal Account

Differentiate between personal and impersonal accounts

Personal Accounts

Personal accounts may be further classified into three categories:

Natural Personal Account

An account related to any individual like David, George, Ram, or Shyam is called as a Natural Personal Account.

Artificial Personal Account

An account related to any artificial person like M/s ABC Ltd, M/s General Trading, M/s Reliance Industries, etc., is called as an Artificial Personal Account.

Representative Personal Account

Representative personal account represents a group of account. If there are a number of accounts of similar nature, it is better to group them like salary payable account, rent payable account, insurance prepaid account, interest receivable account, capital account and drawing account, etc.

Example of personal account

Possessions of the Business

Identify the possessions of the business

Real Accounts

Every Business has some assets and every asset has an account. Thus, asset account is called a real account. There are two type of assets:

- Tangible assets are touchable assets such as plant, machinery, furniture, stock, cash, etc

- Intangible assets are non-touchable assets such as goodwill, patent, copyrights, etc.

Accounting treatment for both type of assets is same.

Nominal Accounts

Since this account does not represent any tangible asset, it is called nominal or fictitious account. All kinds of expense account, loss account, gain account or income accounts come under the category of nominal account. For example, rent account, salary account, electricity expenses account, interest income account, etc.

Impersonal account. any account other than a personal account, being classified as either a real account, in which property is recorded, or a nominal account, in which income, expenses and capital are recorded.

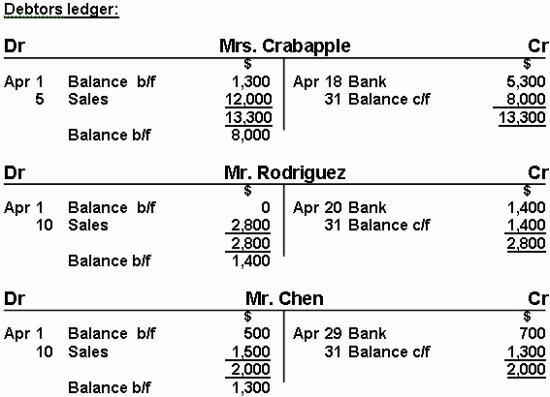

A creditor is an entity or person that lends money or extends credit to another party.

A debtor is an entity or person that owes money to another party. Thus, there is a creditor and a debtor in every lending arrangement. The relationship between a debtor and a creditor is crucial to the extension of credit between parties and the related transfer of assets and settlement of liabilities.

- READ TOPIC 4: Trial Balance